How To Turn An Annual Investment Of $6K Into $5 Million!

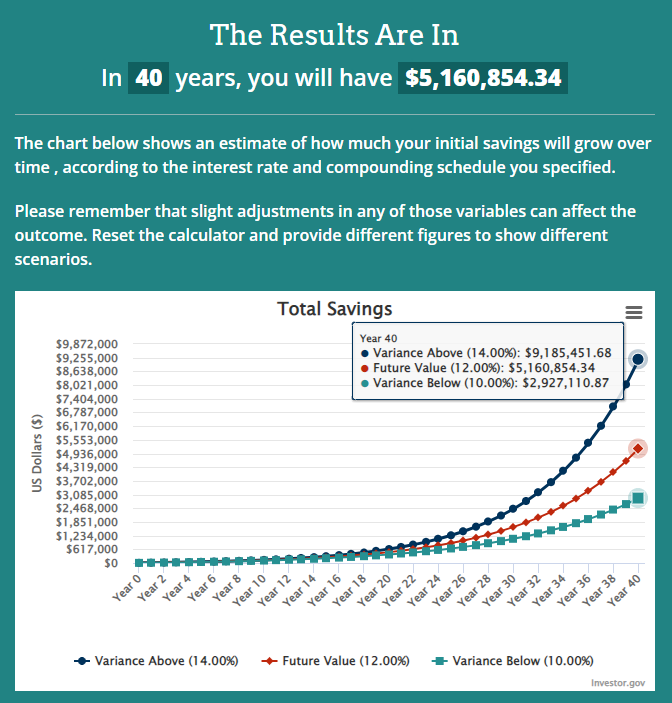

I sat down with my son, Alex, today and told him I set up a self-directed Roth IRA for him. As you can imagine, this was super exciting news for a 19-year-old! What youngster isn’t eager to hear about the money they won’t be able to touch until they are nearly 60 years old BUT, I got his attention when I showed him the graph below. By contributing only $6,000/year (max allowed contribution), a total of $240,000 between now and his retirement age, he can easily have over $5 MILLION by the time he is eligible for retirement!!!

That’s the power of compounded interest, combined with real estate! This is based on a 12% average growth per year, which is the least I make annually on my real estate investments. The graph also shows what happens if it goes up to 14% (easily possible) or if it dips to 10%. In truth, the returns will be much higher than this, because he is investing in real estate syndications that will likely refinance their apartment complexes every 3 to 5 years – returning most of his investment capital at that time. This allows those same funds to be reinvested while maintaining equity in the previously purchased properties. This means, he can reinvest those same funds repeatedly, while still pulling income from the previous investments. For more on how that works, see my rapid wealth growth stratedgy video.

But since the equity and timeline for such things vary, it is impossible to chart that accurately. But what is very clear, is that he will be extremely well off if he follows through with this plan.

BONUS: ALL THAT GENERATED INCOME WILL BE TAX-FREE BECAUSE HE USED A ROTH IRA!

I’m sharing this with you because I wish someone would have showed this to me at an early age.

If you only have 20 years to invest before retirement, to achieve the same results, you will need to start with an investment of $500K – more than twice the total lifetime contribution my son will need to make. Time matters. Sooner is substantially better than later, but today is still better than tomorrow. So, if you’ve been waiting – STOP! Get in the investment game NOW.

P.S. You can do this outside of an IRA, we just choose that avenue to shelter the income from taxes. But there are limits to your annual contributions to an IRA. You can do this through a SOLO 401K that has much greater annual contribution limits if you own your own business and only have 1 employee (yourself). Or you can simply do it with your savings and not worry about the taxes since real estate already provides great tax write-off opportunities.

P.S.S. Create your own chart based on your personal situation (starting contribution amount, annual contributions, and investment years) using this Compound Interest Calculator.

{kind=link}

0 comments

Leave a comment

Please log in or register to post a comment